If you want a Chicago home base without the full-time commitment of a primary residence, the Loop deserves a serious look. For many international buyers, the appeal is simple: you want a well-located downtown condo that supports business travel, city weekends, and easy access to culture without adding unnecessary friction. This guide walks you through what matters most when buying a Loop pied-à-terre, from building rules and rental limits to financing and closing costs, so you can move forward with more clarity. Let’s dive in.

Why the Loop works well

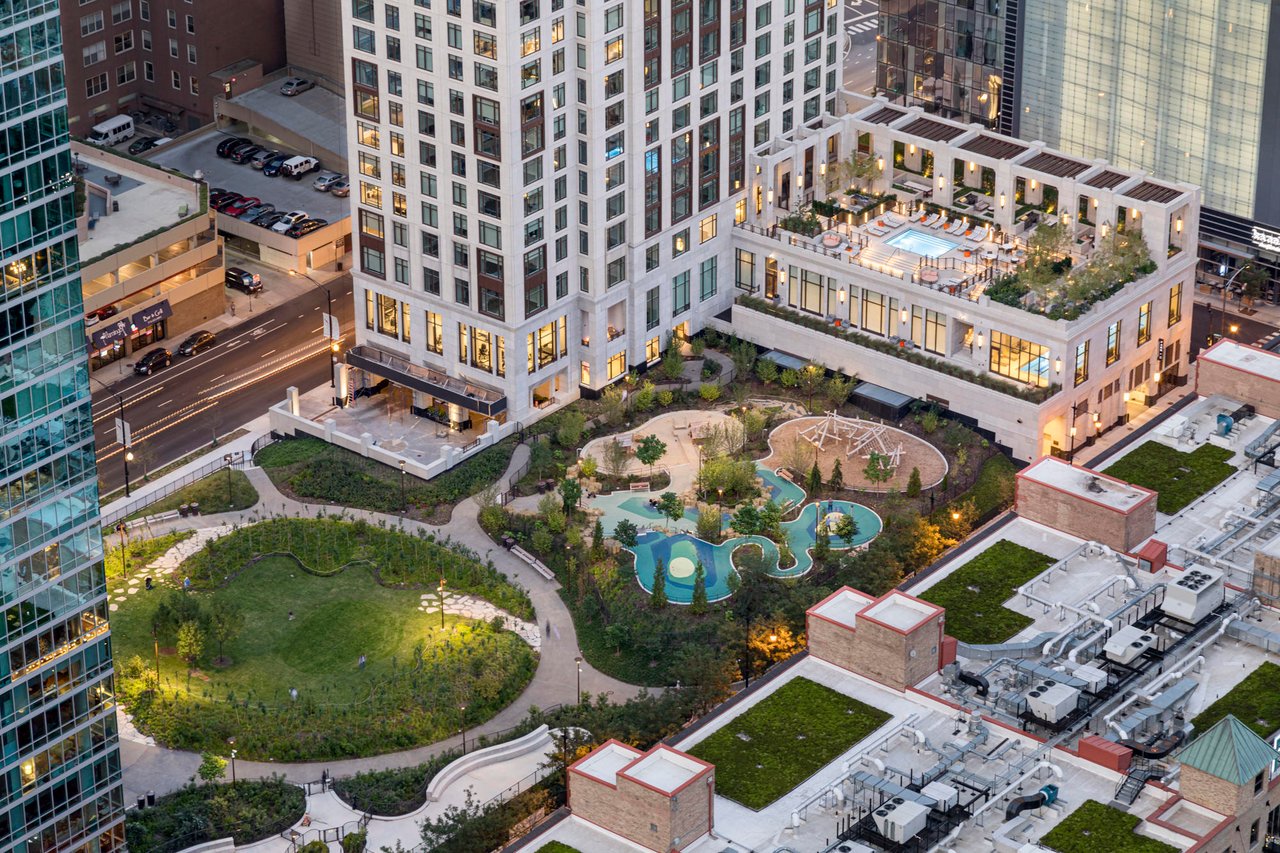

The Loop is Chicago’s official downtown, and that matters when you are buying a part-time residence. It brings together office access, major transit connections, riverfront access, and a dense collection of walkable amenities in one district. If your goal is to land in Chicago and move through the city efficiently, the Loop offers a practical starting point.

It also has a strong cultural identity. Choose Chicago describes the Loop as home to a vibrant theatre district and iconic downtown attractions, and the Chicago Architecture Center notes that the downtown theatre district is concentrated along Randolph Street with landmark venues such as the Chicago Theatre and Cadillac Palace Theatre. For buyers who want a residence that supports both work and leisure, that mix can be especially appealing.

The Loop also sits close to Chicago’s financial core. The Federal Reserve Bank of Chicago is located at 230 South LaSalle Street in the heart of the city’s financial district, which helps explain why the area often attracts executives and global buyers who value convenience near downtown business activity. If you expect to spend meaningful time in the city for meetings, events, or seasonal stays, location efficiency can carry as much weight as the unit itself.

Think lifestyle first

A pied-à-terre is not just a condo purchase. It is a decision about how you want to live when you are in Chicago. Before you compare finishes, views, or amenities, it helps to define how often you expect to use the home and what kind of daily experience you want.

Ask yourself a few practical questions:

- Do you want to walk to offices, restaurants, theaters, and the riverfront?

- Will you be in Chicago for short visits, extended stays, or a mix of both?

- Do you prefer the energy of the central business district or a quieter downtown setting?

- Is rental flexibility important, or is the home strictly for personal use?

These questions matter because the right building for one buyer may be the wrong fit for another. A high-floor condo with dramatic views may look perfect on paper, but if the building rules conflict with how you plan to use it, the lifestyle advantage disappears quickly.

Building documents matter

In Illinois, condo due diligence goes far beyond the unit itself. Under the Illinois Condominium Property Act, the core condominium instruments include the declaration, bylaws, and plat. The law also requires associations to prepare and distribute a detailed annual budget and gives owners the right to inspect major records, including books, minutes, and certain governing documents.

For you as a buyer, that means the paper trail is essential. Before you commit to a Loop pied-à-terre, you should review the building’s governing and financial documents with care. In many cases, these documents will tell you more about long-term fit than a showing ever can.

Start with this checklist:

- Declaration

- Bylaws

- Rules and regulations

- Annual budget

- Reserve information or reserve disclosures

- Insurance summary or certificates

- Recent board meeting minutes

- Leasing policy

- Short-term rental policy

The same Illinois law also requires condominium associations to carry property insurance on the common elements and units at replacement-cost levels, along with commercial general liability coverage. That makes insurance review part of your building-level due diligence, not just a closing detail.

Watch for use restrictions

For an international buyer, usage rules can be deal-critical. A beautiful condo can still be a poor match if the association has strict leasing rules, a strong history of rule enforcement, or policies that limit how often owners can rent or occupy the unit in certain ways. This is especially important if you want flexibility in the future, even if you are buying primarily for personal use today.

In Chicago, rental flexibility is highly building-specific. The city’s shared-housing code makes it unlawful to advertise or rent a shared housing unit if the HOA or board has adopted bylaws prohibiting shared housing or vacation rentals, or if the building owner has prohibited those uses. In larger buildings, Chicago also limits shared-housing use once more than six units or one-quarter of the building, whichever is less, are or will be used as shared housing units or vacation rentals.

Chicago’s restricted residential zones rules can also bar new or additional shared housing units or vacation rentals, including some non-primary-residence uses in certain precincts. On top of that, the city requires a host to register a shared housing unit and include a city-issued registration number before advertising, listing, renting, or booking it for future rental. The practical takeaway is straightforward: if rental flexibility matters to you, never assume it exists just because a unit is in a desirable downtown tower.

How financing may be classified

For many buyers, a true pied-à-terre is most closely aligned with second-home financing rather than primary-residence financing. Fannie Mae states that it purchases and securitizes mortgages for principal residences, second homes, and investment properties. For second-home treatment, the borrower must occupy the property for some portion of the year, the home must be suitable for year-round occupancy, the borrower must have exclusive control over it, and it cannot be rental property, a timeshare, or subject to a management arrangement that controls occupancy.

That distinction matters because it affects your lender conversations from the start. If you intend to use the home personally during part of the year, second-home classification may be relevant. If you expect regular rental use or manager-controlled occupancy, the loan may be treated more like an investment property.

International buyers should also speak with lenders early about documentation. Fannie Mae states that it purchases and securitizes mortgages made to non-U.S. citizens who are lawful permanent residents or non-permanent residents of the United States under the same terms available to U.S. citizens, while leaving documentation decisions to the lender. In practice, that means the lender will determine what is needed to verify legal presence, income, assets, and underwriting eligibility.

What lenders may ask for

Lender requirements vary, but early preparation can make the process smoother. The CFPB says lenders review income, assets, employment status, savings, debts, and credit history or score when deciding whether to lend. If your income, accounts, or tax records span multiple countries, it is smart to start organizing them before you begin serious property tours.

A strong early financing checklist may include:

- Passport and immigration documentation, if applicable

- Proof of income

- Proof of assets and reserves

- Employment verification

- Credit information available to the lender

- A clear explanation of intended occupancy

It is also wise to compare official loan offers rather than relying on informal conversations. The right lender for an international purchase is often the one that can handle your documentation efficiently and explain the path to closing with precision.

Why FHA is usually not the fit

FHA financing is often less relevant for a Loop pied-à-terre. HUD’s Single-Family Housing Handbook says FHA single-family programs are limited to owner-occupied principal residences, and the borrower must occupy the home as a principal residence within 60 days and for the majority of the calendar year. Since a pied-à-terre is commonly a second home rather than a principal residence, conventional, jumbo, or portfolio financing is generally more aligned with this type of purchase.

That does not mean every buyer will use the same loan path. It simply means your financing strategy should match the actual use of the home. Clarity here can prevent wasted time later.

Budget for transfer taxes

Closing costs in Chicago and Cook County are material, so transfer taxes should be part of your planning from day one. Illinois imposes a state real estate transfer tax of 50 cents per $500 of value. Cook County adds 25 cents per $500.

Chicago’s transfer tax structure is more substantial. The city imposes $3.75 per $500 for the city portion plus a $1.50 per $500 CTA supplemental tax. Chicago’s ordinance says the city portion generally falls on the purchaser, while the CTA portion is generally paid by the transferor unless an exemption changes the incidence.

For a luxury condo purchase, these costs can add up quickly. Budgeting for them early helps you evaluate units with a more realistic total-cash picture rather than focusing only on the purchase price.

Plan for Chicago closing logistics

The City of Chicago requires a Full Payment Certificate before the parties can obtain the transfer tax stamps needed to record the deed. That means timing matters. If this step is delayed, recording can be delayed too.

For an international buyer managing travel, banking, and cross-border documentation, smooth execution often comes down to preparation. It helps to treat the closing process as a coordinated checklist rather than a final sprint.

A smart final checklist includes:

- Confirm the building’s leasing policy

- Confirm the building’s short-term rental policy

- Review reserves and insurance

- Finalize lender preapproval or proof of funds

- Budget for state, county, and city transfer taxes

- Start the city Full Payment Certificate process early

- Confirm whether the unit will be delivered furnished or unfurnished

That last point is easy to overlook, but it matters for a part-time residence. If you plan to use the property soon after closing, furniture and move-in readiness can affect your timeline and your budget.

What to prioritize in a Loop pied-à-terre

When you tour Loop condos, the most important factors are usually a blend of lifestyle and structure. You may care about views, natural light, floor height, and building amenities, but those should be evaluated alongside building governance and city rules. The strongest purchase is one where the property feels right and the rules support your intended use.

This is where a high-touch buying process becomes valuable. In a downtown luxury market, details like occupancy classification, building policies, reserve health, and closing logistics can shape the outcome as much as design or location. If you want a Chicago home base that works smoothly from day one, a careful, document-driven approach is worth it.

Buying a Loop pied-à-terre as an international buyer can be a smart move when the building, financing, and use rules align with your plans. If you want discreet, concierge-level guidance on downtown Chicago high-rises and a more strategic buying process, connect with Rafael Murillo for a private consultation.

FAQs

What makes the Loop a good area for a pied-à-terre in Chicago?

- The Loop combines downtown office access, major transit, walkable amenities, riverfront access, and a concentrated theatre district, which can make it especially practical for part-time city living.

What condo documents should you review before buying a Loop pied-à-terre?

- You should review the declaration, bylaws, rules and regulations, annual budget, reserve information, insurance summary, recent board minutes, and any leasing or short-term rental policies.

Can you rent out a Loop pied-à-terre in Chicago?

- It depends on the building’s governing documents and Chicago’s current shared-housing and vacation-rental rules, so rental use should never be assumed without document review.

How is financing different for an international buyer purchasing a Chicago pied-à-terre?

- Lenders may require documentation related to legal presence, income, assets, employment, and occupancy plans, and they decide what is needed for underwriting eligibility.

Is FHA financing a common option for a Loop pied-à-terre?

- FHA is usually a weaker fit because its single-family programs are generally limited to owner-occupied principal residences rather than second homes.

What transfer taxes should you budget for when buying a Loop condo in Chicago?

- You should account for Illinois state transfer tax, Cook County transfer tax, and Chicago’s city and CTA transfer taxes, since these can materially affect total closing costs.